Late Car Payments Hit Highest Level in Decades

More Americans are struggling to keep up with their car payments, reaching the highest delinquency rates in over 30 years. Rising costs and high interest rates have made it increasingly difficult for borrowers to stay current on their auto loans. As financial pressure mounts, many consumers are facing serious consequences, including potential repossession of their vehicles.

Auto Loan Delinquencies Reach Record Highs

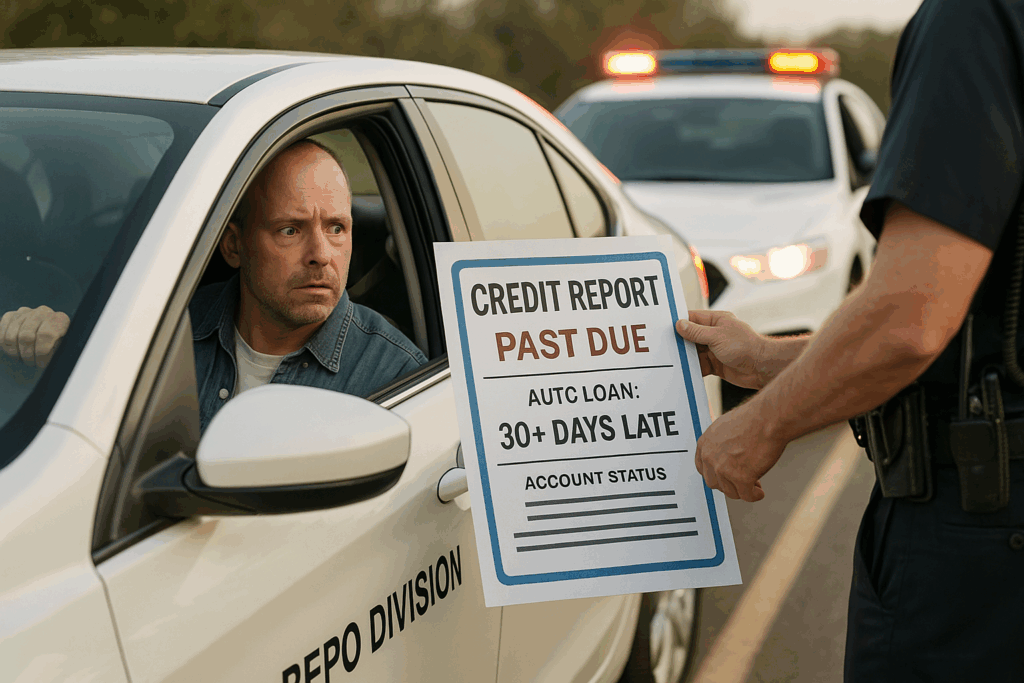

Late car payments hit highest level in decades, with 6.56% of subprime auto borrowers at least 60 days past due on their loans in January. This marks the highest delinquency rate since record keeping began in 1994. The data underscores the growing financial strain many Americans are experiencing as inflation and interest rates remain elevated.

The Federal Reserve Bank of New York also reported a sharp rise in serious delinquencies, which are defined as payments overdue by 90 days or more. In the fourth quarter of 2024, 3% of all auto loans fell into serious delinquency, the highest rate since 2010. The trend suggests that many households are struggling to meet financial obligations, especially when it comes to transportation costs.

Rising Costs Drive Borrowers Into Delinquency

Several factors have contributed to the surge in late car payments. The cost of new vehicles has climbed significantly, increasing from an average of $38,000 in early 2020 to more than $48,500 by January 2025. This $10,000 jump in vehicle prices has made financing more challenging, especially for lower-income and subprime borrowers.

At the same time, late car payments hit highest level in decades due to soaring interest rates. Borrowers now face higher monthly payments, with the average new car loan reaching $755 per month in January 2025. While this figure is slightly lower than the December 2022 peak of $795, it remains well above the pre-pandemic average of $566 in 2019.

Tariffs Could Push Car Prices Even Higher

Economic pressures may worsen as new trade policies take effect. Analysts warn that tariffs on auto imports could drive vehicle prices up by as much as $12,000. The potential increase has raised concerns among both consumers and automakers. To ease the immediate burden, a one-month exemption was granted for auto imports from Mexico and Canada. However, long-term impacts could still make car ownership even more expensive.

Mexico and Canada are major suppliers of vehicles and parts to the U.S., so tariffs could lead to price hikes across the industry. As a result, financing a car may become even more difficult for many buyers, potentially causing further increases in delinquencies.

Who Is Struggling the Most?

Borrowers with lower credit scores are facing the greatest challenges. Fitch Ratings defines subprime auto borrowers as those with credit scores of 640 or below. Among this group, late car payments hit highest level in decades, signaling worsening financial distress.

Meanwhile, prime borrowers—those with higher credit scores—are faring better but are not immune to rising delinquencies. In January 2025, 0.39% of prime borrowers were at least 60 days past due on their car loans, up from 0.35% the previous year. The slight increase suggests that financial pressure is affecting borrowers across all credit tiers, though subprime borrowers remain the most vulnerable.

The Future of Auto Loan Delinquencies

If vehicle prices and interest rates remain high, late car payments could continue to rise. Borrowers who are already struggling may find it even harder to keep up, leading to more repossessions and financial setbacks.

For those at risk, financial experts recommend reviewing budgets, exploring refinancing options, and seeking assistance before missing payments. Lenders may offer hardship programs, but the key is to act early rather than waiting until delinquency occurs.

As late car payments hit highest level in decades, the auto finance industry and policymakers may need to find solutions to prevent further financial strain on consumers. Whether through adjusted lending practices, interest rate relief, or policy changes, addressing the growing auto loan crisis will be critical in the coming months.

If you ever need expert assistance or guidance on your credit journey, don’t hesitate to reach out to the Nerds! Additionally, stay updated with the latest tips and information by following us on Facebook, Instagram and TikTok!